Scope 3 Carbon Emission Standard Revision Framework

The Greenhouse Gas Protocol (GHG Protocol) releases a revised framework for Scope 3 carbon emission standards, aimed at improving Scope 3 data quality, boundary setting, and investment activity accounting.

The GHG Protocol launched the Scope 3 carbon emission standard revision in 2024, aiming to enhance the completeness, consistency, transparency, and comparability of corporate carbon emissions while considering feasibility.

Related Post: ISSB Sets a Grace Period of One Year for Scope 3 Disclosure

Background of Scope 3 Carbon Emission Standard Revision

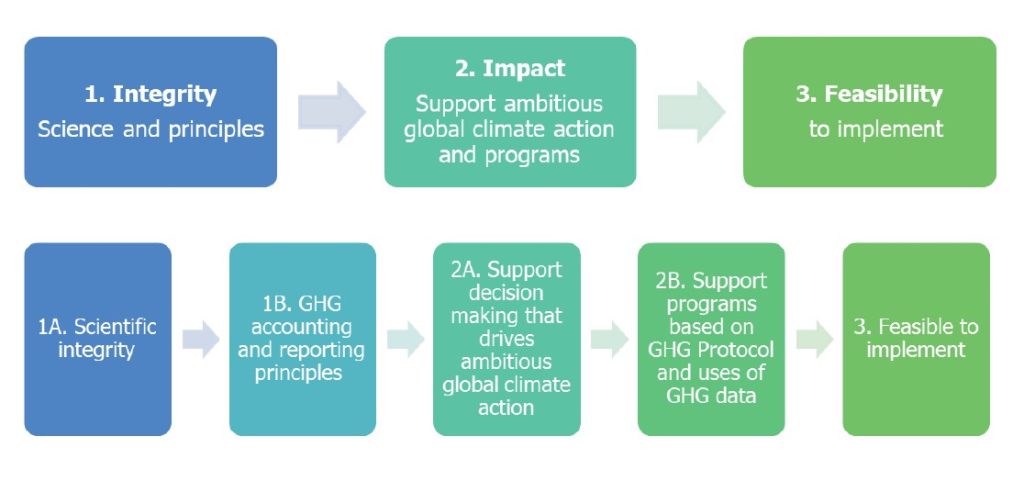

The revision of Scope 3 carbon emission standards is managed by the GHG Protocol Secretariat and developed by the Scope 3 Technical Working Group. It is reviewed by the Independent Standards Board. The priority considerations for the revision process include:

- Integrity: Maintain scientific integrity and principles of carbon emission accounting and disclosure.

- Impact: Support global climate action.

- Feasibility: Consider the feasibility of implementing standards.

This revision is divided into three parts, namely:

- Series A Revision (Data Quality and Related Topics): Increase data transparency, improve data quality, and enhance data reliability.

- Series B Revision (Boundary Setting): Introduce clear thresholds, optimize integrity guidelines, and enhance the rigor of carbon emissions.

- Series C Revision (Classification and Disclosure Requirements for Investment Activities): Clearly define the accounting scope of Category 15 investment activities and improve the consistency of their classification, calculation, and disclosure.

Introduction to Scope 3 Carbon Emission Standard Revision

The report introduces the revised content from the three series mentioned above:

The core objective of Series A revisions is to address Scope 3 data quality and transparency issues by introducing new disclosure requirements to encourage businesses to collect higher quality data. The revised content of Series A is as follows:

- Decompose emissions by data type: The current standard requires companies to disclose the total amount of Scope 3 by category and describe the data type, source, method, and other information used. The new standard requires companies to disclose data according to each Scope 3 category and decompose it into different levels of disclosure based on different data types (industry average data, input-output data, etc.).

- Implement disclosure audits: The current standard recommends that companies disclose the types, qualifications, and opinions of third-party audits in appropriate circumstances. The new standard requires companies to disclose whether Scope 3 overall data is fully audited, partially audited, or unaudited.

- Improve data quality: The new standard recommends that companies use high integrity emission factors, set mid-term or annual data quality improvement goals, and set performance indicators for Scope 3 (such as the proportion of Scope 3 data calculated based on first-hand data).

The core goal of Series B revisions is to introduce new thresholds and categories to make Scope 3 boundaries clearer, more consistent, and comprehensive. The revised content of Series B is as follows:

- Introduce minimum boundary requirement: The current standard requires companies to account for all Scope 3 carbon emissions and disclose any excluded items. The new standard requires companies to account for and disclose at least 95% of Scope 3 carbon emissions, with the excluded portion not exceeding 5%.

- Update disclosure justification requirements: The new standard requires companies to disclose and justify any excluded Scope 3 carbon emissions and use specific disclosure negative signs (such as NA indicating not applicable) to mark the excluded items and requires companies to disclose Scope 3 carbon emissions and optional Scope 3 carbon emissions separately.

- Add Category 16 of carbon emissions: The new standard introduces an optional Category 16 of carbon emissions, namely other value chain activities. The Category 16 of carbon emissions mainly applies to financial enterprises that earn trading income but may never purchase, sell, or own such third-party activities (such as brokerage activities engaged by financial enterprises).

The core objective of Series C revision is to clarify the accounting scope and classification standards for Category 15 carbon emissions (investment activities). The revised content of Series C is as follows:

- Narrow down the definition scope of Category 15: The current standard considers all enterprises with investments to be included in Category 15, while the new standard narrows the scope to financing emissions, and other non-financing emissions are included in the newly added Category 16 carbon emissions.

- Clear calculation boundary: The new standard requires all investment activities in Category 15 to be included in the calculation and requires that the accounting boundary must include Scope 3 data of the investees. The 95% minimum threshold requirement also applies but provides reasonable exclusion clauses for specific financial instruments for businesses to choose from.

- Introduce new disclosure requirements and reference standards: The new standards require companies to disclose the percentage of the book value of their Category 15 investments to the total book value of financial assets, to improve transparency. The new standard suggests that companies refer to industry-specific standards, such as the Partnership for Carbon Accounting Financials (PCAF), when distinguishing between financing emissions and non-financing emissions activities.

Reference: