Climate and Nature Risk Management Practice Report

The European Central Bank (ECB) releases a report on climate and nature risk management practices, aimed at providing financial institutions with methods to incorporate climate and nature risks into their strategic, governance, and risk management processes.

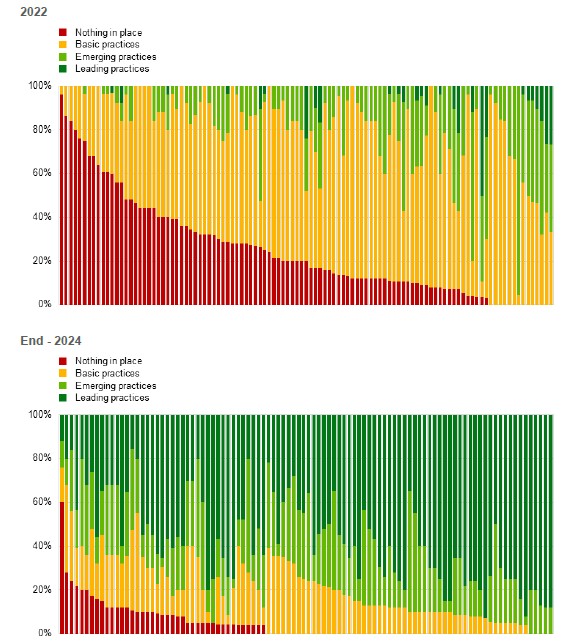

The European Central Bank believes that financial institutions should shift from simple risk identification to forward-looking prudent transition plans, while managing risks and seeking business opportunities brought about by transition.

Related Post: CDP Releases 2026 Corporate Climate and Nature Progress Report

Climate and Nature Risk Management Practice: Strategy

Strategy is the foundation for financial institutions to achieve long-term development. In climate and nature risk management, financial institutions can focus on:

- Prudent Transition Plan: Financial institutions need to assess their transition risk exposure, set strategic goals for substantive risks, and divide long-term goals (such as net zero commitments) into medium-term goals and short-term goals (such as industry policies). Financial institutions can set Key Performance Indicators and Key Risk Indicators to measure progress.

- Customer Transition Plan: Evaluate the transition plan from the production plan and technology roadmap provided by the customer, link the evaluation results with customer risk classification, and apply them to business decision-making. For customers with higher risks, financial institutions can demand higher risk premiums or provide financing opportunities with restrictive conditions.

- Transitional Products and Services: Develop transitional financial products to support clients undergoing transition. For example, providing sustainable development linked credit linked to customer carbon emission reduction performance indicators.

Climate and Nature Risk Management Practice: Governance

Effective governance institutions are important factors in ensuring the implementation of risk management strategies, and financial institutions can pay attention to:

- Board of Directors: The board of directors is responsible for risk management, such as approving transition plans, setting risk appetite, and ensuring that they have sufficient knowledge and experience. Financial institutions can regularly provide training to their board of directors.

- Organizational structure: Establish three different governance departments, namely the business department, compliance department, and audit department. The business department is responsible for identifying, assessing, and managing risks in daily operations, the compliance department is responsible for developing risk management policies, monitoring risk exposures, and the audit department is responsible for evaluating the effectiveness of the risk management framework.

- Risk preference framework: Incorporate climate and nature risk management into the risk preference framework and setting key risk indicators.

Climate and Nature Risk Management Practice: Risk Management

Climate and nature risks are the driving factors of traditional risks, and financial institutions can pay attention to:

- Materiality assessment: Establish a systematic process to identify how climate and nature risks affect traditional risks. For example, extreme weather events can create physical risks that may lead to a decrease in collateral value and credit risk.

- Customer due diligence and risk classification: Collect customer level data such as carbon emissions, energy consumption, geographic location, and transition plans. Use this information to classify customers’ risks and monitor whether their business involves dispute activities.

- Valuation of collateral and credit pricing: Consider climate and nature risks in collateral valuation and incorporate risk costs into credit pricing. For example, providing preferential interest rates for green projects and charging higher risk premiums to customers with high transition risks.

- Capital adequacy ratio and stress testing: Incorporate climate and nature risks into the internal capital adequacy assessment process, such as estimating potential credit losses under the impact of extreme climate events through stress testing and assessing long-term risk exposure.

Reference:

Good Practices for Advancing Climate and Nature-related Risk Management