This article introduces the EU Corporate Sustainability Due Diligence Directive (CSDDD).

The EU Corporate Sustainability Due Diligence Directive will gradually be applied in the coming years, imposing mandatory social and environmental due diligence requirements on eligible EU and non-EU enterprises.

Timeline of EU Corporate Sustainability Due Diligence Directive

On February 23, 2022, the European Commission released a proposal for a sustainable due diligence directive for enterprises, which was submitted to the Council of the European Union and the European Parliament. On December 1st, the European Council passed the proposal. On December 14, 2023, the European Parliament and the European Council reached a provisional agreement on Corporate Sustainability Due Diligence Directive.

On March 15, 2024, the European Council issued a revised version of the Corporate Sustainability Due Diligence Directive. On April 24th, the European Parliament passed the revised version, and on May 24th, the European Council officially adopted the revised Directive, which was published in the Official Journal of the European Union on July 5th. The directive officially came into effect on July 25th. EU member states need to enact it into their own laws before July 26, 2026.

Related Post: The EU Adopted Corporate Sustainable Due Diligence Directive

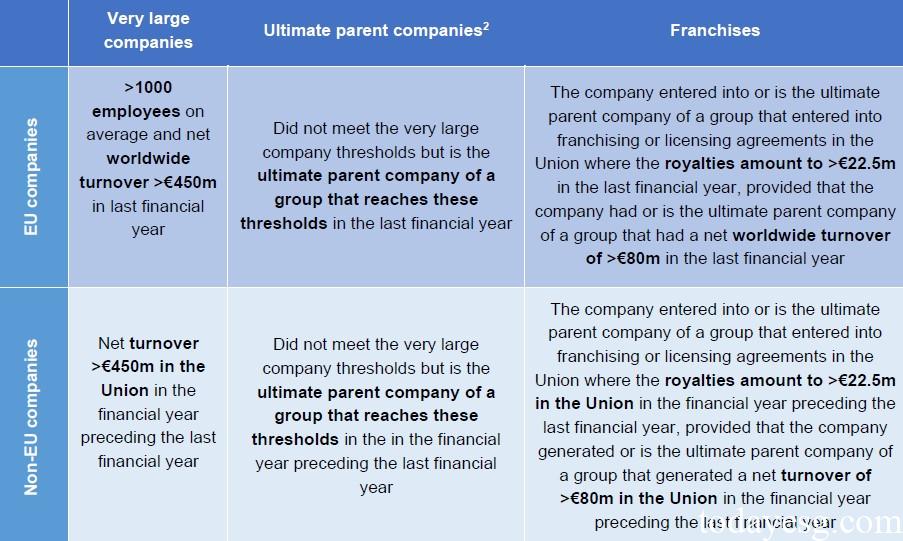

Introduction to EU Corporate Sustainability Due Diligence Directive

The EU Corporate Sustainability Due Diligence Directive aims to ensure that enterprises operating in the EU contribute to the sustainable transition of the economy and society. It requires enterprises to ensure that their business models comply with global warming targets and take responsibility for actual and potential adverse social and environmental impacts. At present, CSDDD include:

- EU companies with an average of over 1000 employees and a turnover of over 450 million euros or parent companies operating in the EU.

- Non-EU enterprises with a turnover of over 450 million euros or parent companies operating in the EU.

Eligible enterprises are required to conduct social and environmental due diligence, including:

- Incorporate due diligence into policies and risk management systems: Companies need to incorporate due diligence into their policies and risk management systems, and develop a separate due diligence policy, including due diligence methods, code of conduct, and measures taken by the policy. Enterprises also need to review and update their due diligence policies every two years.

- Identify and evaluate actual or potential adverse impacts: Enterprises need to take appropriate measures to identify and evaluate the actual or potential adverse impacts generated by themselves, subsidiaries, or partners in business activities. Enterprises can draw operational maps to identify which areas are most likely to experience these impacts and conduct in-depth evaluations.

- Prevent or mitigate adverse impacts: Enterprises need to take appropriate measures to prevent or mitigate existing or potential adverse impacts, including developing action plans and timelines, using indicators to measure adverse effects, seeking third-party verification, etc. In necessary circumstances, enterprises may also suspend or terminate related businesses.

- Establish and maintain notification mechanisms and complaint procedures: Enterprises should establish notification mechanisms and complaint procedures, allow individuals or organizations to file complaints, and handle these complaints openly, fairly, and transparently.

- Monitor the effectiveness of due diligence policies and measures: Enterprises need to regularly evaluate their own, subsidiary, and business partner operations in order to assess the adequacy and effectiveness of due diligence and make appropriate modifications to any unrealistic measures.

- Public communication on due diligence: Companies need to issue an annual statement explaining their compliance with CSDDD. The EU will develop a template for this declaration in 2027.

Corporate Sustainability Due Diligence Directive and Climate Transition Plan

The EU CSDDD stipulates that all eligible enterprises are also required to develop climate transition plans to ensure that their business activities are aligned with sustainable economic transition and meet the warming targets of the Paris Agreement. The transition plan should include:

- Based on scientific evidence, the 2030 mid-term carbon reduction target and 2050 net zero target, as well as the Scope 1, Scope 2, and Scope 3 carbon emission data involved in these targets.

- The key actions taken by enterprises to achieve the above goals, such as product and service adjustments and new technologies application.

- The funds and resources invested by enterprises in climate transition plan, as well as the roles of various departments in it.

The CSDDD requires companies to update their climate transition plans annually and summarize their progress for the year. When a company develops a climate transition plan based on the CSDDD, it can also be considered compliant with the requirements of the Corporate Sustainability Reporting Directive (CSRD).

Reference:

Investor Briefing: EU Corporate Sustainability Due Diligence Directive