Nature Guidelines for CFOs

The Taskforce on Nature-related Financial Disclosures (TNFD) releases nature guidelines for CFOs, aimed at helping businesses identify, assess, and address nature related issues, and incorporate natural factors into their core financial processes.

This guide starts with natural core issues, covering aspects such as understanding, assessing risk opportunities, integrating natural factors, and financial planning.

Related Post: Sustainable Stock Exchanges Initiative Releases Nature-related Financial Disclosures Guidance

Impact of Nature on Enterprise Financial Performance

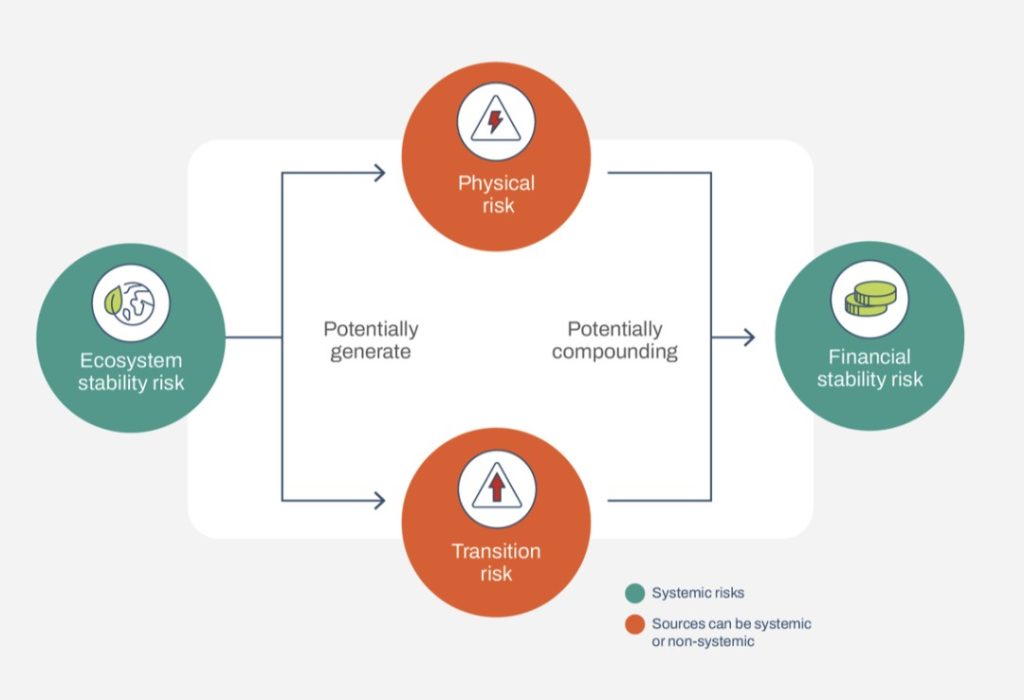

Changes in nature, biodiversity, and ecosystems may have an impact on a enterprise’s financial performance. Corporate financial performance often relies on nature, such as the benefits provided by nature (such as industrial raw materials, soil, and water resources) and corporate activities (such as deforestation). As a key infrastructure supporting operation, changes in nature may directly lead to increased costs, operational disruptions, increased supply chain vulnerability, and decreased productivity.

For CFOs, the natural impact on an enterprise’s financial performance includes:

- Income and expenditure: How an enterprise’s dependence and impact on nature can potentially affect its income and expenditure.

- Assets and liabilities: How nature affects asset valuation and asset impairment.

- Capital allocation: Whether nature has been included in the capital plan and strategic investment decisions.

Assessment of Nature Risks and Opportunities in Enterprises

Nature risks are usually divided into physical risks (such as water scarcity) and transitional risks (such as regulatory policy changes), which can be identified and evaluated through the LEAP method published by the TNFD. The CFO needs to pay attention to whether the risk management team has identified and understood the natural risk types related to the enterprise, and whether they have been incorporated into the existing risk management process. Scenario analysis is also an effective method for enterprises to identify and quantify natural risks. Enterprises can extend existing climate scenarios to factors such as biodiversity loss and water resource pressure.

Nature dependencies and impacts also bring about opportunities, such as new sources of income, cost savings, etc. The CFO needs to identify the driving factors of natural related opportunities and evaluate them based on financial and strategic substance. In decision-making, enterprises can use exclusion criteria (such as not affecting local biodiversity) or use shadow pricing to evaluate funding expenditures. The performance of enterprises in natural aspects can also help them obtain new sources of financing (such as sustainable bonds) and reduce the cost of capital.

Enterprise Nature Information Disclosure

Natural regulation and information disclosure are related to the jurisdiction, but overall disclosure requirements are increasing. Investors also hope to obtain more natural related risk disclosure, management, and other information. The CFO needs to understand these regulatory policies, including understanding the expectations of key stakeholders, market trends, and existing sustainable disclosure frameworks. Nature related data is often scattered across operations and value chains, and some require estimation and access to third-party information, posing challenges to information disclosure.

The CFO needs to evaluate whether the existing system can stably store, manage, and report natural data, and refer to climate related financial disclosure methods to transform complex natural information into effective insights for business decision-making.

Reference: