ISSB Standard Readiness Guidelines

IFRS releases ISSB Standard Readiness Guidelines in jurisdictions, aimed at helping for the application of ISSB standards in jurisdictions.

Since the release of IFRS S1 and IFRS S2 in 2023, IFRS has issued various guidelines and roadmaps to ensure that jurisdictions can provide high-quality sustainable financial information disclosure.

Related Post: ISSB Releases Preview of the Inaugural Jurisdictional Guide for the Adoption of ISSB Standards

Background of ISSB Standard Readiness Guidelines

IFRS believes that jurisdictions will go through the following stages before the formal application of ISSB standards:

- Familiar with ISSB standards.

- Evaluate the reasons for adopting ISSB standards and consider the level of preparation.

- Develop a roadmap for the application of ISSB standards.

- Implement the roadmap.

This guide mainly focuses on the second stage, where jurisdictions need to consider the readiness of key ecosystem participants (such as regulators, professionals, data providers) and enterprises, as well as the readiness of supporting systems such as accounting firms and partners. The functions of these evaluations include:

- Provide decision-making basis for the development of ISSB standard roadmap for jurisdictions.

- Provide insights that may affect regulatory actions, scope, and sequence.

- Obtain information and evidence for cost-benefit analysis.

- Determine the key areas of ecosystem capacity building and technical support needs.

Introduction to ISSB Standard Readiness Guidelines

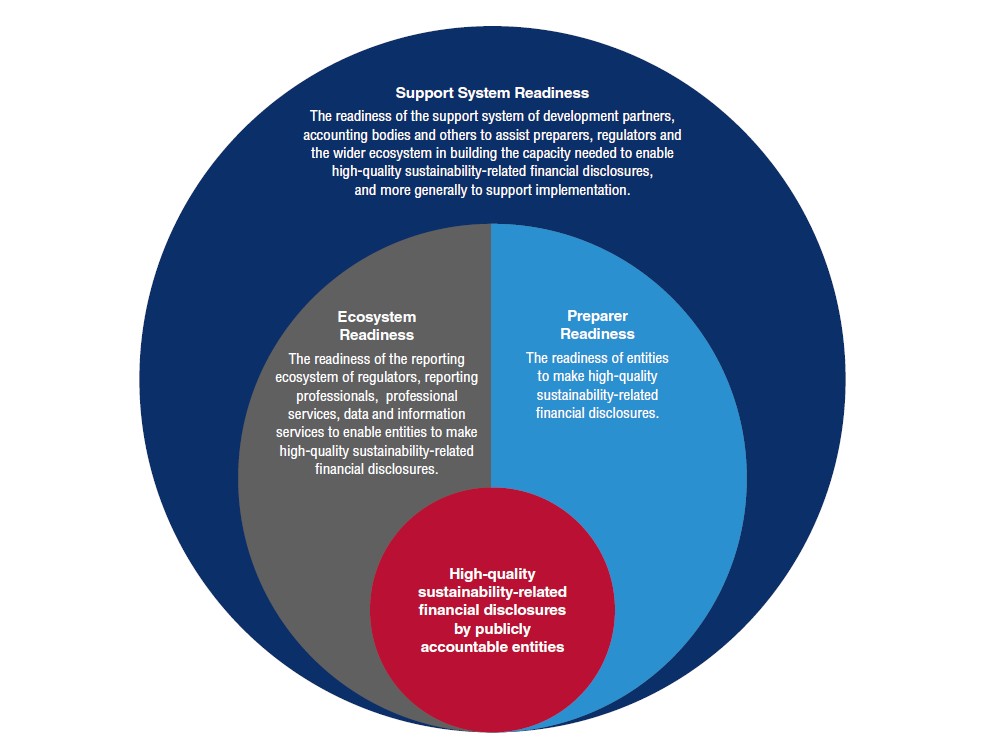

IFRS divides ISSB Standard Readiness Guidelines into three interrelated parts:

- Part 1: Ecosystem readiness, which refers to the level of readiness of market infrastructure to support high-quality and sustainable financial information disclosure.

- Part 2: Enterprise readiness, which refers to the level of readiness of enterprises to provide high-quality and sustainable financial information disclosure.

- Part 3: Support system readiness, which refers to the readiness of ecosystems and enterprises to release high-quality sustainable financial information disclosure.

Each part contains the following contents:

- Part 1 Regulatory Framework and Institutional Basis: Jurisdictions need to have the authorization, resources, technology, and operational capabilities to introduce, supervise, and enforce sustainable financial disclosures. These foundations can enhance investors’ confidence in sustainable disclosure.

- Part 1 Professionals and Services: High quality disclosure depends on professional information disclosure consultants and auditors who translate regulatory obligations into practice, provide strategic and technical guidance, and ensure disclosure integrity and credibility.

- Part 1 Information and Data Infrastructure: Information infrastructure such as datasets, industry benchmarks, emission factors, and scenarios can improve the quality of reports and shorten the time frame for writing reports.

- Part 2 Maturity, Skills, and Professional Competence: Enterprises need to have experience in identifying, assessing, and managing sustainable development related risks and opportunities, as well as professional sustainable development skills and abilities.

- Part 2 Disclosure Requirements Familiarity and Reporting Practices: Enterprises need to have a detailed understanding of IFRS accounting standards, IFRS S1 and IFRS S2 standards, as well as international frameworks such as climate disclosure and carbon emissions disclosure.

- Part 3 Support System: Jurisdictions need to consider the financial, technical, information, and capacity assistance that international institutions, multilateral development banks, accounting firms, and other technical partners can provide.

IFRS believes that jurisdictions can use various readiness assessment methods based on their specific circumstances, prioritize issues with insufficient readiness, and use this information in the development of the ISSB standard application roadmap. As industry develops, jurisdictions need to regularly reassess their readiness to meet investors’ needs for sustainable information.

Reference:

Jurisdictional Readiness Assessment Guide and Tool Added to ISSB Adoption Toolkit