ESG Ratings and Data Products Report

The International Capital Markets Association (ICMA) releases a report on ESG ratings and data products, aimed at summarizing the development, market applications, and regulatory policies of ESG ratings and data products.

This report is based on a survey conducted by the ICMA on asset owners and asset managers, with a total AUM of $28 trillion.

Related Post: International Capital Market Association Releases Code of Conduct for ESG Ratings and Data Products Providers

ESG Ratings and Data Products Overview

Although ESG ratings and data products were initially classified as non-financial data, their financial materiality and impact have been accepted by the market. The survey shows that investors use ESG services provided by an average of six suppliers, which is significantly higher compared to credit ratings (averaging two to three suppliers). In addition to ESG ratings and ESG data, some suppliers also provide services such as ESG dispute event reports, ESG indices, and Second Party Opinions on sustainable bonds.

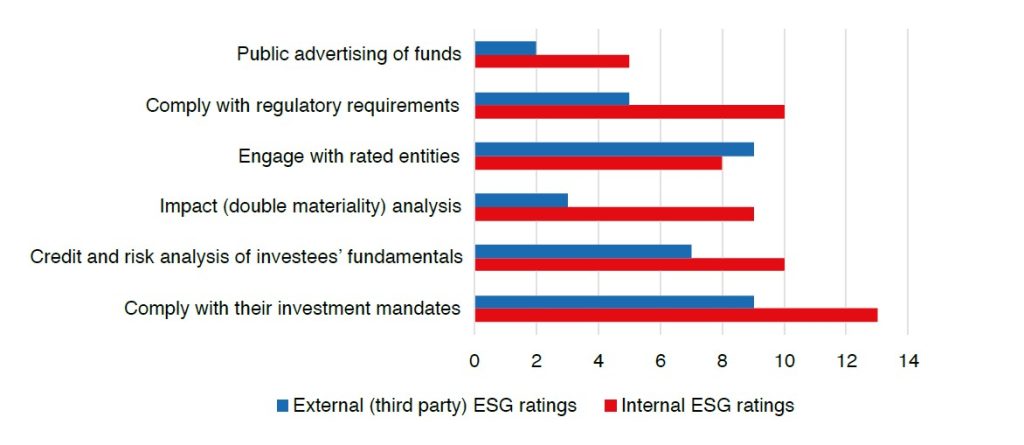

Respondents are using external ESG services while also creating internal ESG products based on professional methodologies and models. The reasons for developing internal ESG products include reducing reliance on external products, improving transparency and consistency, and adapting to specific investment strategies. The survey shows that almost all asset managers have established internal ESG ratings systems. External ESG products are mainly used to comply with investment authorization and due diligence, while internal ESG products mainly analyze investees.

ESG Ratings and Data Products Regulation

The increasing importance of ESG ratings and data products has prompted regulatory agencies to continue paying attention. In 2018 EU Sustainable Finance Expert Group believes that sustainable ratings agencies are important information intermediaries and recommends the development of requirements to improve the clarity and transparency of information. The International Organization of Securities Commissions (IOSCO) released a consultation document in 2021, proposing ten recommendations on governance, quality, independence, transparency, and encouraging regulatory agencies to develop voluntary codes of conduct. In 2022, the International Organization of Securities Commissions released ESG ratings and data products supplier practice documents, providing specific case studies.

Under the recommendation of the International Organization of Securities Commissions, the International Capital Market Association released the ESG Ratings and Data products Supplier Code of Conduct in 2023, enhancing market integrity in six directions. This code of conduct is an important reference for regulatory agencies to formulate policies, such as the regulatory document released by the Securities and Futures Commission of Hong Kong in October 2024. According to a survey by FTSE Russell, over 50% of asset owners believe that the code of conduct issued by the International Capital Market Association significantly improves market transparency and has a positive impact on ESG ratings and data products regulation.

ESG Ratings and Data Products Development

The International Capital Market Association believes that the following factors will affect the future development of ESG ratings and data products:

- The relationship between voluntary codes of conduct and mandatory regulation: Since the International Organization of Securities Commissions proposed ten recommendations, ESG ratings and data products providers have improved the transparency of their methodologies and internal processes. However, ESG products still need to provide more detailed information to their subscribers. In this context, the EU has proposed two types of disclosure: disclosure to the public and disclosure to subscribers. In the implementation of voluntary codes of conduct, regulatory policies need to strike a balance between disclosing and protecting commercially sensitive information.

- Standardization of sustainable disclosure: The application of the International Sustainability Standards Board (ISSB) standards can improve quality, consistency, and comparability of sustainable disclosure. This standard can assist ESG data providers in obtaining and processing data. However, recent simplification of regulatory policies in various jurisdictions may affect the scope and availability of sustainable data. The ISSB standards reserve the discretion of each jurisdiction, which may lead to a decrease in the scope and quality of ESG data disclosure in the future.

- Differentiation of ESG ratings: ESG ratings are more complex than credit ratings, as providers use different methodologies and ratings scales, resulting in significant differences in ESG ratings. In addition, credit ratings can be verified through external events, and the verification ability of ESG ratings is relatively low. Some investors believe that differentiation in ESG ratings is beneficial and can assist in conducting more detailed analysis. Other investors believe that differentiation in ESG ratings is not conducive to enhancing usability. Investors typically use ESG ratings from multiple providers and compare the ESG ratings methodologies of different providers.

Reference: