Bond Market Green Premium Report

The European Central Bank (ECB) releases a report on bond market green premium, aimed at summarizing the characteristics of green premiums.

The ECB analyzes 9500 green bonds issued globally from 2014 to 2023 and matches over 250000 non-green bonds based on their characteristics.

Related Post: What is Greenium? Why does it exist?

Background of Bond Market Green Premium

The core difference between green bonds and non-green bonds is that the funds raised are typically used to support projects that achieve environmental goals. Green bonds have a negative spread compared to traditional bonds, indicating that environmentally friendly projects have financing advantages. There are significant differences in the estimation of green premiums in existing literature, which may range from a few basis points to several tens of basis points. The ECB believes that in addition to the green label of green bonds, investors may also pay attention to the issuer’s sustainable characteristics. In this case, the premium of green bonds may vary among different bond types and issuers.

The ECB uses Coarsened Exact Matching to group the key control variables of bonds, including issuance year, amount, maturity, currency, credit rating, country, and industry. Within each group, the ECB matches multiple non-green bonds with the same characteristics for each green bond and uses regression analysis to study the bond green label premium, issuer environmental disclosure premium, and the relationship between the two.

Analysis of Bond Market Green Premium

The regression analysis results of the green premium in the bond market include:

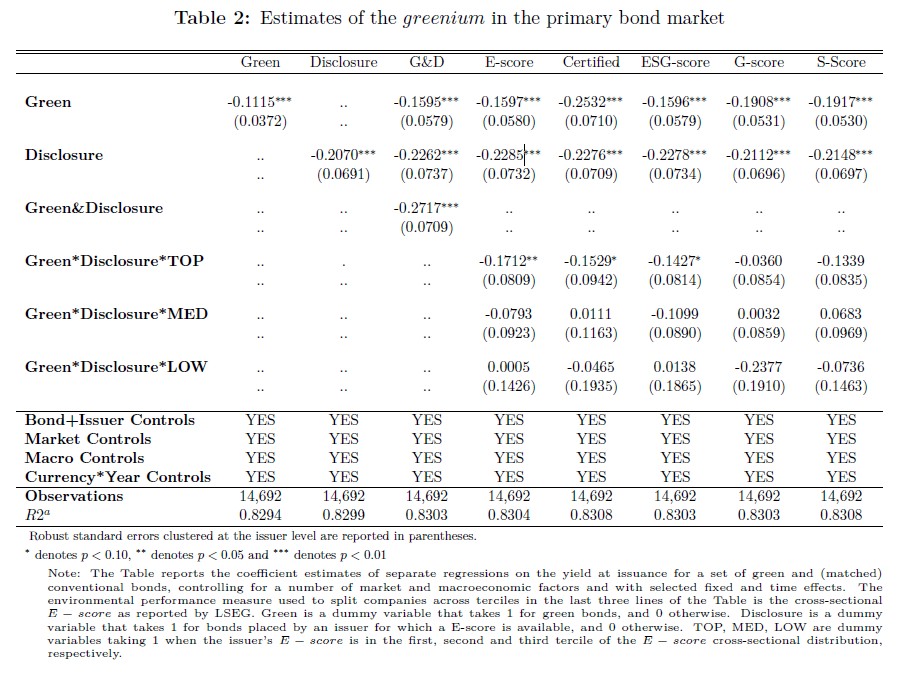

- Green label premium for bonds: With a green label, green bonds have a green premium of 16 basis points at the time of issuance. Regardless of whether the issuer has environmental disclosure, investors prefer green bonds.

- Issuer environmental disclosure premium: If the issuer can provide environmental information disclosure, its issued bonds (whether green or non-green) can receive a premium of 23 basis points. This indicates that environmental disclosure can reduce the financing costs of issuers.

- The relationship between green label premium and environmental disclosure premium: When green label and environmental disclosure coexist, the premium will significantly expand. For example, if the green label premium is 16 basis points, when the issuer’s environmental rating is in the top one-third of the total sample, the total premium will increase from 16 basis points to 33 basis points. When the issuer’s environmental rating is not in the top one-third of the total sample, the total premium remains at 16 basis points. This indicates that investors will prefer issuers with better environmental performance.

Excluding the above premium types, when green bonds obtain third-party certification, their premium can increase from 16 basis points to 25 basis points, indicating that third-party certification can also provide a similar role for issuers in environmental disclosure.

Green Premium and Climate Risk Awareness

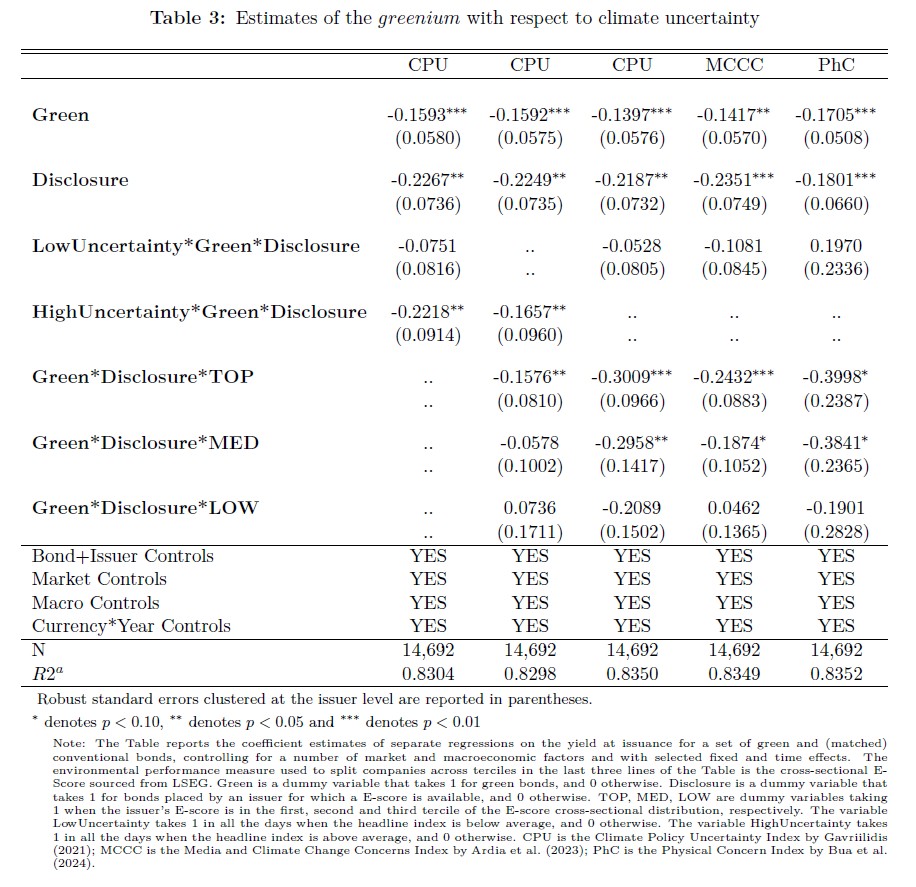

The ECB analyzes how changes in investors’ climate risk awareness affect green premiums. Investors’ climate risk awareness is divided into high-risk awareness period and low-risk awareness period:

- High-risk awareness period: During this period, the green premium is more pronounced. When the issuer’s environmental rating is in the top one-third of the total sample, the total premium will expand from 33 basis points to 44 basis points. If the issuer’s environmental rating is at a moderate level of the total sample, the total premium will also increase from 16 basis points.

- Low-risk awareness period: During this period, the green premium will shrink, and only the top one-third of issuers will receive a premium, with a total premium of 33 basis points. Bonds issued by other issuers will not receive additional green premiums.

The ECB believes that investors will simultaneously pay attention to the use of bond funds and the issuer’s environmental disclosure and have a higher preference when climate risks rise. Even issuers with low environmental performance can obtain green premiums if they finance green projects. Some high emission enterprises can also receive positive financial support during the transition process.

Reference: