Consultation on Sustainable Disclosure of Listed Companies

The UK Financial Conduct Authority (FCA) releases a consultation on sustainable disclosure of listed companies, aiming to adjust the existing sustainable disclosure framework to comply with ISSB international standards.

The UK Financial Conduct Authority believes that the existing Sustainability Reporting Standards for listed companies are based on the Taskforce on Climate-related Financial Disclosures (TCFD). As global jurisdictions gradually adopt the International Sustainability Standards Board (ISSB) standards, this adjustment can improve the interoperability and consistency of sustainability disclosure.

Related Post: UK Financial Conduct Authority Plans to Revise Sustainability Disclosure Requirements

Sustainable Disclosure Framework for UK Listed Companies

To evaluate the applicability of ISSB standards, the UK released a draft sustainable disclosure standard for public opinion in June 2025, making some modifications to the international standard to meet the actual situation. The draft for soliciting opinions divides the sustainable disclosure standards into two parts, namely SRS S1 and SRS S2, which correspond to IFRS S1 and IFRS S2 respectively. SRS S1 recommends that listed companies refer to various international guidelines, such as the Sustainability Accounting Standards Board (SASB) standards, and propose key concepts applicable to all sustainability themes.

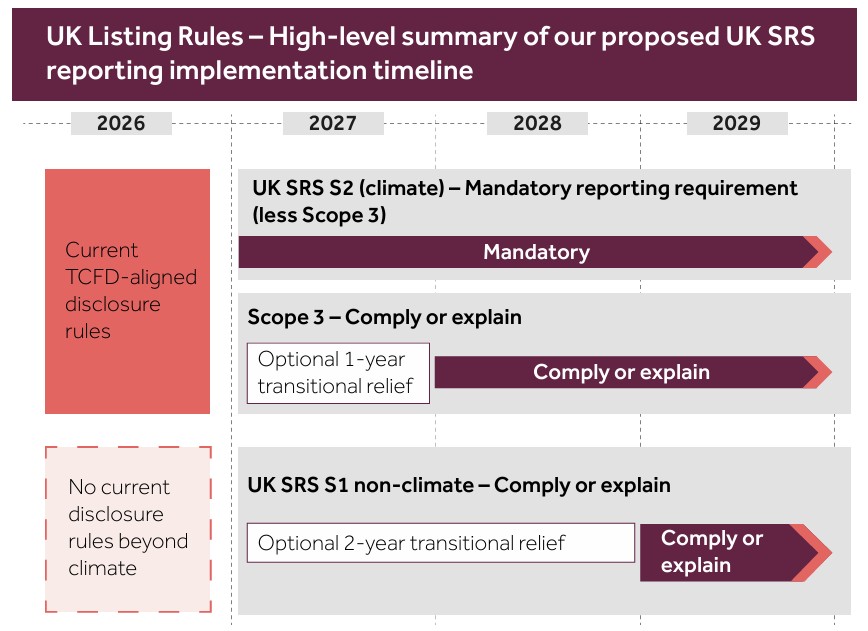

SRS S2 proposes specific requirements for climate-related risks and opportunities, in line with the recommendations of the TCFD. Market participants’ feedback shows that listed companies face challenges in Scope 3 disclosure due to difficulties in collecting carbon emission data from third parties. The regulatory authorities plan to reduce the compliance burden of enterprises through a transitional period while improving the quantity and quality of sustainable information, to meet the information needs of investors.

Adjustments to Sustainable Disclosure of Listed Companies

The UK Financial Conduct Authority plans to adjust the sustainable disclosure framework for listed companies in the following areas:

- Disclosure scope: The scope of application of the sustainable disclosure framework is consistent with existing enterprises, mainly including commercial companies, secondary listed companies, depositary receipts, non-equity joint stock companies, etc. Closed end investment companies and open-ended investment companies do not need to disclose.

- Climate Disclosure: Involving SRS S2. Existing listed companies are already quite mature in terms of climate disclosure, and the consultation requires companies to disclose climate-related information compulsorily. Considering the disclosure challenges raised by market participants regarding Scope 3, companies can adopt the principle of compliance or interpretation, either disclose Scope 3 or explain the reasons for non-disclosure.

- Non-climate disclosure: Involving SRS S1. For sustainable topics beyond climate, such as biodiversity and water resources, most listed companies lack sufficient experience. Therefore, consultation requires companies to adopt principles of compliance or interpretation rather than mandatory disclosure. This is also the first time that this principle has been introduced in non-climate disclosure, while climate disclosure continues this principle.

- Transition Plan: ISSB standards do not require companies to develop and disclose transition plans. The consultation believes that the transition plan has value for investors, therefore listed companies need to disclose whether they have formulated a transition plan, and if not, explain the reasons.

- Sustainable audit: Like the requirements of the transition plan, companies need to disclose whether they have obtained third-party audits for non-climate disclosures and climate disclosures. If an audit has already been obtained, it is necessary to disclose the audit provider, audit scope and category, audit standards, and the method of obtaining audit results.

- International issuers: For international issuers whose primary listing location is not in the UK, the consultation requires them to use the sustainable disclosure framework of their primary listing location to disclose information and disclose their existing transition plans and sustainable audits.

Implementation of Sustainable Disclosure of Listed Companies

The UK Financial Conduct Authority plans to officially release a sustainable disclosure framework in January 2027, which will take effect from the accounting year starting in January 2027. In terms of the transition period, the consultation provides a one-year grace period for Scope 3 disclosure, meaning that compliance or interpretation principles will take effect in January 2028. The consultation provides a two-year grace period for non-climate disclosure, which means compliance or interpretation principles will take effect in January 2029.

The UK Financial Conduct Authority believes that the new sustainable disclosure framework for listed companies will improve market efficiency, help investors allocate funds effectively, and reduce the cost of capital for listed companies. Market participants can continue to provide feedback, and regulatory agencies will release official documents in the third quarter of 2026.

Reference:

Aligning Listed Issuers’ Sustainability Disclosures with International Standards